Section 47 of the Income Tax Act, 1961 (India) specifies transactions that are not regarded as transfers for the purposes of capital gains tax. Under normal circumstances, when a capital asset is transferred, any gains or profits derived from the transfer are subject to capital gains tax. However, Section 47 provides exemptions for certain types of transactions, making them tax-free.

Following transactions are not regarded as transfer. Therefore, no Capital Gain will arise

1. Distribution of capital asset on the partial or total partition of HUF [Section 47(i)]

2. Transfer of capital asset under gift, will, irrevocable trust [Section 47(ii)]

*Note:

This clause shall not apply to gift or an irrevocable trust of share, debenture or warm allotted by company to employee under ESOPS.

As per sixth proviso to Section 48- FMV on the date of transfer (date of GIFT or irrevocable trust) shall be treated as FVOC of such shares, debentures or warrants.

3.Transfer of capital asset by holding company to its subsidiary company or subsidiary to its holding provided following conditions are satisfied [Section 46(iv)/Section 47(v)]

Holding company holds 100% shareholding of subsidiary company

Transferee company should be Indian company

In above cases

(A) Cost of Acquisition Section 49 (1): Cost to the previous Owner

(B) Cost of Improvement: Incurred by previous owner & present owner shall be considered.

(C) Period of Holding: POH of previous owner shall also be considered.

(D) Indexed Cost of Acquisition: Manjula J. Shah (Bombay H.C)

Cost of Acquisition X Cost Inflation Index of the year of Transfer/Cost Inflation Index for the year in which asset first held by Previous Owner

(E) Benefit of Fair Market Value as on 01/04/2001

4. Transfer under Amalgamation

Transfer of Any Capital asset by Amalgamating company to amalgamated company

If Amalgamated Company is an Indian Company

5.Transfer under Demerger

Transfer of Any Capital asset by Demerged Company to Resulting Company

If resulting Company is a Indian Company

6.Conversion of Securities

Conversion of Bond, Debentures, Debenture stock, Deposit certificates of a company into Share or debenture of same company Section 47(x)

Cost of Acquisition of share/debenture on conversion = cost of that part of bond, debenture deposit certificates which is converted Section 49(2A) Period of holding of share/ debenture shall also include the period for which bond, debenture, deposit certificates held by assessee

Conversion of Preference share of a company into equity of same company Section 47(xb)

Cost of Acquisition of equity share received on conversion = cost of that part of preference shares which is so converted Section 49(2AE) Period of holding of equity share shall also include the period for which preference shares held by the assessee Section(42A)

Conversion of gold into electronic gold receipt (EGR) issued by a Vault Manager, or conversion of Electronic Gold Receipt into Gold Section 47(viid) (Added by finance Act,2023 With effect from AY 2024-2025)

Cost of Acquisition of current asset (EGR/gold) received on conversion = cost of earlier asset (EGR/gold) which is so converted Section 49(10) Period of holding of (EGR/gold) shall also include the period for which preference shares held by the assessee Section(42A)

7.Transfer of Sovereign Gold Bond issued by RBI under Sovereign Gold Bond Scheme 2015, by way of redemption by the assessee being an Individual. (Section 47)

8. Transfer of Work of Art, scientific, archaeological, manuscript, books, photograph or print to Govt., University, National Museum or art gallery or archives, any public notified museum. Section 47(ix)

9. Transfer of capital asset under reversed mortgage under a scheme made and notified by CG. Section 47(xvi)

*Note: Amount of loan (either in instalment or lumpsum) received by the senior citizen under the transaction of reverse mortgage would be exempt from income tax u/s 10(43).

Starting a startup is a thrilling journey, especially in India. Its vibrant ecosystem is full of entrepreneurial opportunities. However, to move from idea to execution, you need the right tools in your arsenal. Whether you’re working on a tech innovation, a service platform, or a product-based Startup, leveraging these tools can simplify the process and maximize your efficiency.

This blog will explore tools in several categories. They are for idea validation, project management, marketing, finance, and more. They will help you build your startup dream.

Idea Validation Tools: Test Before You Leap

Before investing time and money into your idea, ensure it’s market-ready.

SurveyMonkey: Create surveys to gauge public interest in your product or service.

Google Trends: Understand market demand and trends in your industry.

Typeform: Engage potential customers with interactive forms and questionnaires.

Project Management Tools: Stay Organized

Execution requires meticulous planning and coordination, especially when managing a team.

Trello: Organize your tasks using a simple Kanban board. Ideal for small teams.

Asana: Plan, track, and manage projects effectively with team collaboration features.

Slack: Streamline communication with your team through instant messaging and integrations.

Financial Tools: Manage Money Like a Pro

Financial management is crucial for startups, especially during the early stages.

QuickBooks: Keep track of expenses, invoices, and cash flow seamlessly.

Razorpay: A payment gateway solution tailored for Indian businesses.

Zoho Books: A GST-compliant accounting tool for Indian startups.

Marketing and Growth Tools: Build and Grow Your Audience

Effective marketing is the key to attracting customers and building a strong brand.

Canva: Design stunning graphics for your website, social media, and ads.

HubSpot: Manage your CRM, email marketing, and analytics in one place.

Google Ads and Facebook Ads: Reach your target audience through paid advertising.

Productivity Tools: Work Smarter, Not Harder

Boost individual and team productivity with the right tools.

Notion: Combine notes, tasks, and databases in one tool.

Google Workspace: Access Gmail, Docs, Drive, and Calendar for seamless work.

Grammarly: Ensure every communication piece is free from grammatical errors.

Legal and Compliance Tools: Stay on the Right Side

Navigating the legal landscape in India can be challenging. These tools simplify compliance:

Counselvise: Get help with company registration, GST filings, and legal templates and much more.

IndiaFilings: Handle legal documentation and compliance effortlessly.

ClearTax: A comprehensive tax filing and compliance platform.

Funding and Networking Platforms: Build Your Base

Finding investors and networking is critical for startups.

AngelList India: Connect with investors and co-founders.

LinkedIn: Network with industry professionals and potential partners.

LetsVenture: A platform to pitch ideas and secure funding from angel investors.

Startup India: A government initiative offering mentorship, resources, and funding opportunities.

Learning and Skill Development Platforms: Stay Ahead

Continuous learning is essential for navigating the evolving business landscape.

Coursera: Learn business, technology, and management skills from top universities.

Udemy: Access affordable courses tailored for entrepreneurs.

Y Combinator Startup School: Free programs for early-stage founders.

India’s startup ecosystem is rapidly growing. With the right tools, you can tackle challenges and seize opportunities. From validating your idea to managing your finances and marketing your product, these tools are your trusted allies.

Tools can boost efficiency. But, your passion, resilience, and innovation will drive your startup’s success.

So, what are you waiting for? Start building your dream startup today!

In the ever-evolving landscape of taxation, receiving a Goods and Services Tax (GST) notice can be both perplexing and daunting. However, taxpayers can navigate the situation with confidence if they understand these notices. This guide gives an updated overview of GST notices. It covers common triggers, types, communication modes, response strategies, and the risks of inaction.

What is a GST Notice?

A GST notice is an official communication dispatched by tax authorities to taxpayers, highlight potential compliance issues or soliciting additional information. These notices serve as instruments to ensure adherence to GST laws and prompt corrective measures when discrepancies arise.

Common Reasons for Receiving GST Notices

Taxpayers might encounter GST notices for several reasons, including:

Mismatches between GSTR-1 (outward supplies) and GSTR-3B (summary return) can raise red flags.

Overstated or ineligible ITC claims may attract scrutiny.

Delay in filing of GSTR-1 and GSTR-3B consecutively for more than six months

Divergences between e-way bill data and GST returns can prompt inquiries.

Operating without requisite GST registration when mandated by law.

Non-payment of GST liability (tax) or the short-payment of the tax with or without the intent to defraud: show cause notice (SCN)

Types of GST Notices and Appropriate Responses

Sr. no

Name of the Form- Notice

Description

Reply or Action to be taken

Time limit to respond

Consequence of non- response

1.

GSTR-3A

Issued to non-filers of GST returns such as GSTR-1, GSTR-3B, GSTR-4, or GSTR-8.

File the pending returns promptly, accompanied by applicable late fees and interest.

Within 15 days from the date of notice issuance.

Tax authorities may proceed with a best judgment assessment. The penalty will be applicable of Rs. 10,000 or 10% of the tax due, whichever is higher.

2.

CMP-05

A show-cause notice questioning the taxpayer’s eligibility for the Composition Scheme.

Justify eligibility by providing necessary explanations or documents as to why the taxpayer should continue to be eligible for the composition scheme.

Within 15 days of receiving the notice.

The penalty stipulated under section 122 and order in CMP-07 denying the benefit of composition scheme

3.

REG-03

Issued during GST registration or amendment, seeking additional information or clarification.

Submit the required information or documents in Form REG-04.

Within 7 working days from the date of receiving notice.

Rejection of the GST registration or amendment application and inform the applicant electronically in REG-05.

4.

REG-17

A show-cause notice by the officer for potential cancellation of GST registration due to specified reasons.

Provide with the reasons for non-cancellation of GST registration in Form REG-18.

Within 7 working days from the date of receiving notice.

Cancellation of GST registration in REG-19

5.

REG-23

Show cause notice why the cancellation of GST registration must be revoked, seeking clarification regarding the proposed cancellation of the taxpayer’s GST registration.

Respond by submitting a reply in Form REG-24, providing justifications for why the GST registration should not be canceled.

Within 7 working days from the date of receiving the notice

Cancellation of GST Registration will be revoked

6.

PCT-03

Issued to GST practitioners for alleged misconduct or breach of professional duties.

Provide a suitable explanation or defense against the allegations.

As specified in the notice.

Suspension or cancellation of the GST practitioner’s license.

7.

RFD-08

Issued when there is a discrepancy or issue with a refund application.

Address the concerns raised by providing additional information or rectifying errors in RFD-09

Within 15 days of receipt of notice

Make an order in RFD-06 for rejecting the GST Refund application

8.

ASMT-02

Issued when additional information, clarification, or documents are required for provisional assessment.

Provide the requested information or documents in ASMT-03

Within 15 days from the date of service of this notice

Application for provisional assessment may be rejected

9.

ASMT-06

Issued when additional information, clarification, or documents are required for final assessment.

Submit the necessary information or documents to assist in the final assessment in ASMT-07

Within 15 days from the date of service of this notice

The final assessment may be completed without considering the taxpayer’s perspective, potentially resulting in unfavorable outcomes.

10.

ASMT-10

Issued when discrepancies are identified in the returns filed by the taxpayer

Reply in ASMT-11 giving reasons for discrepancies in the GST returns

Within 30 days from the date of notice issuance.

The tax authority may proceed with an assessment based on available information, potentially leading to additional tax liabilities and penalties.

11.

ASMT-14

Issued under Section 63 of the CGST Act when a taxpayer has not registered despite being liable for registration or when a registered person fails to file returns, leading the tax authority to propose a best judgment assessment.

Reply in written form and appear before the GST authority issuing the notice

Within 15 days of notice

Failure to respond within the stipulated time can lead the tax authority to proceed with the best judgment assessment, which could result in higher tax liabilities.

12.

ADT-01

Issued when tax authorities decide to audit the taxpayer’s records.

Cooperate with the audit process by providing the requested documents and information.

Within the time prescribed in the notice

Non-compliance may result in penalties and a more detailed investigation by the tax authorities

14.

DRC-01

Issued for tax demand due to discrepancies or audit findings.

Reply in DRC-03 for paying the amount of tax demanded in the notice along with Interest and penalty, if any applicable. Use DRC-06 to reply to the show cause notice

Within 7 days of receiving the notice.

Initiation of recovery proceedings.

15.

DRC-10

Issued for the auction of goods under Section 79(1)(b) of the CGST Act due to non-payment of dues.

Settle the outstanding dues immediately to prevent the auction of goods.

Before the auction date specified in the notice. Note that the last day of the bid or the last day of the auction cannot be before 15 days from the date of issue of the notice

Auctioning of the taxpayer’s goods to recover dues.

16.

DRC-13

Issued to a third party under Section 79(1)(c) of the CGST Act, directing them to pay any amount due to the defaulting taxpayer directly to the government.

The third party must comply by remitting the specified amount to the government.

Not applicable

The third party may face legal consequences for non-compliance.

17.

DRC-16

Notice for attachment and sale of immovable/ movable goods/ shares under section 79

A taxpayer receiving this notice is prohibited from transferring or creating a charge on the said goods in any way and any transfer or charge created by you shall be invalid

Not applicable

Any contravention of the notice can invite prosecution and/or penalties

Valid modes of sending GST Notices

Tax authorities employ various channels to dispatch GST notices, including:

Hand-delivering the notice either directly or by a messenger by a courier to the taxpayer or his representative.

By registered post or a speed post or a courier with an acknowledgement- addressed to the last known place of the business of the taxpayer.

Communication to the email address

Making it available on the GST portal after logging in.

publication in a regional newspaper circulated in the locality- that of the taxpayer based on the last known residential address.

If the tax authorities do not use any of the above means, they must affix it in a prominent place at the person’s last known business or residence. If they do not find this reasonable, they can affix a copy on the notice board of the concerned officer’s or authority’s office as a last resort.

Consequences of Ignoring GST Notices

Neglecting GST notices can lead to severe repercussions, such as:

Monetary Penalties: Fines imposed for non-compliance or delayed responses.

Interest Accruals: Accumulation of interest on unpaid tax liabilities.

Legal Proceedings: Initiation of legal action, including prosecution in cases of serious violations.

Business Disruptions: Suspension or cancellation of GST registration, hindering business operations.

Reputational Damage: Tarnishing of the business’s reputation due to perceived non-compliance.

At Counselvise we have designed NoticeBoard to help you keep track of all your client’s notices. It helps you-

Automate notice retrieval from Income Tax & GST portals

Centralize all notices in one dashboard

Track deadlines & receive timely reminders

Use AI-powered suggestions for easy responses

Staying informed about GST regulations and maintaining diligent compliance practices are key to navigating the complexities of GST notices effectively.

Income tax notices are official communications from the Income Tax Department to a taxpayer, highlighting issues or actions related to their tax filings. Receiving such a notice doesn’t always indicate wrongdoing; it may simply request additional information or clarification.

Types of Income Tax Notices

Section

Purpose

Description

139(9)

Defective Return Notice

Issued when the filed return is found defective or has discrepancies. Taxpayers are required to rectify the defects within a specified timeframe.

142(1)

Inquiry Before Assessment

Sent when the Assessing Officer requires additional information or documents to complete the assessment process.

143(1)

Intimation Notice

An intimation after processing your return, indicating any discrepancies or confirming that the return has been accepted as filed.

143(2)

Scrutiny Notice

Issued if the department selects your return for detailed scrutiny to verify the correctness of the declared income and claimed deductions.

148

Income Escaping Assessment

Sent when the department believes that some income has escaped assessment, requiring the taxpayer to file a revised return.

156

Notice of Demand

Issued when any tax, interest, penalty, or other sum is payable, specifying the amount due.

245

Set Off Refunds Against Tax Remaining Payable

Informs the taxpayer that their refund is being adjusted against existing tax liabilities

Notice u/s 139(9) – Defective Income Tax Return

In this case, if the Assessing Officer is of the opinion that the ITR filed by the assessee is defective then he may issue notice u/s 139(9). The Assessing Officer also shares the proper error description along with the probable solution to rectify the same. The defect u/s 139(9) can be because of the wrong ITR filed, wrong or non-declaration of Income as per Form 26AS, missing information, incomplete return, etc.

The Assessing Officer gives the Assessee an opportunity to respond within 15 days from the date of intimation. If the Assessee fails to respond within the stipulated time, the Assessing Officer considers the return invalid and proceeds with the assessment.

Assessee may agree or disagree with the observation of the Assessing Officer. If you can agree, you can file a return after rectifying the defect in the return.

Notice u/s 142(1) – Inquiry Before Assessment

The purpose of this notice is to request additional information and documentation from the taxpayer to complete the processing of their filed return. The authorities will also send this notice to compel the taxpayer to furnish additional documents and details. Also, if the Assessee has not filed their return on time, they will receive a notice for a preliminary inquiry u/s 142(1). The time limit to serve the notice u/s 142(1) is before the end of the relevant assessment year.

Notice u/s 143(1) – Intimation

Notice u/s 143(1) is one of the most common income tax notices that is frequently received by taxpayers from the income tax department, it requires a response to rectify errors, incorrect claims, or inconsistencies in a filed income tax return. If an individual receives this notice and wishes to amend their return, they have a 15-day window to do so. Otherwise, the authorities will process the tax return after incorporating the necessary adjustments specified in the notice.

Notice u/s 143(2) – Scrutiny

If the Assessing Officer deems the Assessee’s response to the Income Tax Notice u/s 142(1) unsatisfactory or if the Assessee fails to provide the requested documents, the officer issues a notice u/s 143(2).

There can be 3 types of following notices under Section 143(2):

Limited Scrutiny: Under Limited Scrutiny, the system selects cases through Computer-Assisted Scrutiny Selection (CASS) based on set parameters. The scrutiny focuses solely on the specific area of the return mentioned in the notice. An example of this scrutiny can be a mismatch in tax credits, inaccurate information, etc.

Complete Scrutiny: The authorities conduct a complete scrutiny of the filed return along with all supporting documents. The system flags cases based on CASS, and the scope of scrutiny extends beyond these types of notices. However, the assessing officer cannot verify documents beyond the particular assessment year.

Manual Scrutiny: Cases are selected for complete scrutiny based on the criteria defined by the Central Board of Direct Taxes; the criteria may vary every year.

Taxpayers who receive notice under Section 143(2) will have to submit additional information. The Assessee or their authorized representative may file a reply through the portal, as physical submissions are no longer required. The process will be conducted exclusively through E-Assessment.

Notice u/s 148 – Income Escaped Assessment

In such cases, the assessing officer has the authority to assess or reassess the income. Before proceeding with the assessment or reassessment, the officer must serve a notice to the assessee requesting them to provide their income return. This notice is issued under Section 148 of the income tax provisions.

Notice u/s 156 – Demand Notice

If any penalty, tax, fine, or other amount is due from the taxpayer to the Income Tax Department, the authorities will serve an Income Tax notice u/s 156. This notice is typically issued after the assessment of the ITR. The taxpayer must deposit the amount payable within 30 days from the date of the notice. There is no specific time limit to serve this notice. Income Tax notices u/s 143(1) and 200A are also referred to as Notice of Demand.

Notice u/s 245 – Refund Adjusted against the Tax Demand

It is basically an Intimation from the Income Tax Department. The authorities issue this notice when they adjust a tax refund (full or partial) for an assessment year against the tax demand due from the taxpayer. If the assessing officer suspects tax evasion in previous years and decides to offset the current year’s refund against the outstanding demand, they may issue a notice u/s 245.

The authorities can make such an adjustment only after giving the individual proper notice and an opportunity to be heard. The notice recipient must respond within 30 days of receiving it. If they fail to respond, the assessing officer may treat it as implied consent and initiate the assessment process accordingly. Therefore, it is advisable to respond to the notice promptly.

The assessment year of refund and tax demand can be different. There is no time limit to serve or send Income Tax Notice / Intimation u/s 245.

How to resolve such notices

Type of Notice

Steps to Resolve

Section 143(1) – Intimation Notice

– Verify the details mentioned in the notice. – If no errors, no action is required. – If discrepancies exist, respond to the notice within 30 days.

Section 139(9) – Defective Return Notice

– Review the defects mentioned. – Correct the return and re-submit it within the specified period.

Section 142(1) – Inquiry Before Assessment

– Provide the requested documents/information within the time frame. – Seek an extension if required.

Section 143(2) – Scrutiny Notice

– Respond with the requested documents and explanation. – Co-operate with the assessing officer. – If needed, seek professional help for complex cases.

Section 148 – Income Escaping Assessment

– Review the notice and reasons for reassessment. – File the revised return or provide clarification within the deadline. – Seek professional advice if needed.

Section 156 – Notice of Demand

– Pay the demanded tax within the specified time or file an appeal if there is a dispute. – If unable to pay, request for instalment payment.

Section 245 – Set Off Refunds Against Tax Due

– Ensure all tax dues are cleared. – Check if any refunds due are being adjusted. – Respond to the notice, if necessary, for any discrepancies.

General Tips for Resolving Income Tax Notices:

Read the Notice Carefully: Understand the reason for the notice and the required action.

File Responses on Time: Missing deadlines can lead to penalties.

Seek Professional Help: If the case is complex, it is advisable to consult a tax professional or CA.

Maintain Proper Documentation: Always have the necessary documents ready, such as tax returns, receipts, and other supporting documents.

How to Check Notices on the Income Tax Portal

Follow the steps mentioned below to reply to different income tax notices:

Step 1: Visit the income tax E-Filing Portal

Step 2: Log in to the E-Filing portal using your user ID and password.

Step 3: Go to the ‘e-File’ menu and Check for any notices in your account.

Step 4: On your Dashboard, click Pending Actions > e-Proceedings.

Step 5: On the e-Proceedings page, click Self.

Steps to Reply to Income Tax Notices:

Read the Notice Carefully:

Understand the nature of the notice, such as whether it is for an inquiry, scrutiny, demand, or any other reason.

Check the due date for response and other specific instructions in the notice.

Collect Required Documents:

Gather all relevant documents that may support your claim or rectify any errors in your filed return. These could include:

Previous year’s tax returns

Income proof (salary slips, bank statements, etc.)

Expense documents (bills, receipts, etc.)

Tax payment receipts

Any communication from the tax department (if applicable)

Prepare a Response:

For Defective Return Notices (Section 139(9)): Correct the errors in the return and submit the revised return.

For Scrutiny Notices (Section 143(2)): Submit the documents asked for (e.g., income details, supporting evidence for deductions, etc.) along with an explanation.

For Income Escaping Assessment (Section 148): Provide clarification or submit a revised return if applicable.

For Demand Notices (Section 156): If the demand is valid, make the payment or file an appeal if there is a dispute. If you cannot pay the full amount, request for instalment payment options.

Draft a Reply Letter (if applicable):

Write a formal letter to the Income Tax Department, explaining your position and attaching the required documents. Use a clear and concise format.

Include your PAN, assessment year, and other details as mentioned in the notice to ensure the department can link the response with the correct case.

If you’re filing an appeal or requesting additional time, mention that in the letter.

File the Response Online (if applicable):

For many types of notices, you can file the response directly through the Income Tax Department’s e-filing portal.

Go to the “e-File” section.

Choose the appropriate form (e.g., “Response to Notices”).

Upload the required documents and submit.

For physical submission, send the response to the local Income Tax office that issued the notice.

Pay Tax or Penalty (if applicable):

If the notice demands payment of tax, ensure that you pay the demanded amount before the deadline to avoid penalties and interest.

You can pay through the Income Tax Department’s online payment portal or using challan forms (ITNS 280).

Acknowledge Receipt of Notice:

If replying in person, make sure to get an acknowledgment for the documents submitted.

If submitting online, keep a record of the submission confirmation and a copy of the documents uploaded.

Follow-Up (if necessary):

Follow up with the tax office if you do not receive a response or if further clarification is needed.

Monitor the status of your case through the e-filing portal or contact the department directly.

At Counselvise we have designed NoticeBoard to help you keep track of all your client’s notices . It helps you-

Automate notice retrieval from Income Tax & GST portals

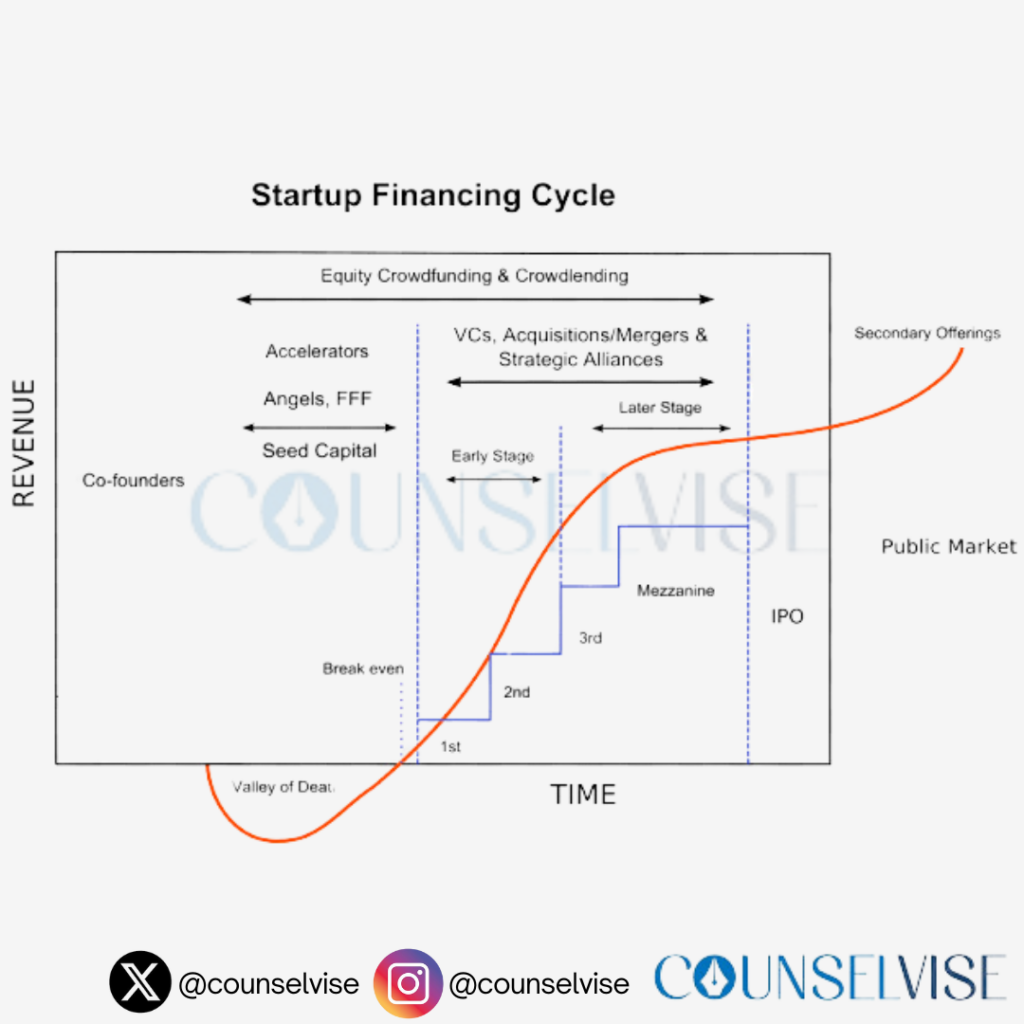

Navigating the complex world of startup financing can be one of the most challenging aspects for entrepreneurs. Understanding the various stages of startup funding is crucial for securing the right capital at the right time. Each stage serves a specific purpose in the lifecycle of a startup and attracts different types of investors. In this detailed guide, we’ll explore the key funding stages, the types of investors involved, and how to position your business for success.

Bootstrapping (Self-Funding): The Starting Point of Your Journey

Bootstrapping is often the first step in the funding journey. In this phase, founders use their own personal savings, credit cards, or loans from family and friends to finance their startup. This method gives you full control of the company. But, it has big financial risks. You are personally liable for any debts.

While bootstrapping can be a viable option for founders with the necessary funds, it’s essential to weigh the risks. In the early days, most of the capital goes toward prototyping, market research, and getting the business off the ground. Since the founder is the sole investor at this stage, a solid financial plan is vital. It will help avoid burning through personal resources.

Advantages of Bootstrapping:

Full control and ownership of the company.

No need to share profits or decision-making power.

You remain independent from outside investors.

Disadvantages of Bootstrapping:

Significant personal financial risk.

Limited funds may slow down growth and scaling.

Lack of external validation from investors.

Pre-Seed Funding: Validating Your Idea

The pre-seed stage is when a startup is still in its infancy. Now, the focus is on refining the business idea, doing market research, and developing a prototype or Minimum Viable Product (MVP). This stage is critical. It validates the business concept before larger investments.

Funding in this stage typically comes from personal savings, close friends and family, or early-stage angel investors. Angel investors, who are typically successful entrepreneurs or professionals, invest their own capital in exchange for equity. They are often interested in the potential of the idea and the founder’s vision rather than the financial metrics.

Advantages of Pre-Seed Funding:

Provides necessary capital to develop and test the idea.

Allows founders to validate the business concept before pursuing larger investments.

Attracts angel investors who can also offer mentorship and guidance.

Disadvantages of Pre-Seed Funding:

Small amounts of capital may limit growth potential.

Investors may expect high levels of involvement or control.

No guarantee that the idea will attract further funding.

Seed Funding: Taking Your Idea to Market

Once your startup has a validated product or service, seed funding is the next step. Seed funding allows businesses to scale operations, build a customer base, and create a more refined version of their product or service. Seed funding is crucial for businesses looking to take their MVP to market.

At this stage, angel investors, early-stage venture capitalists , and crowdfunding platforms often provide the needed capital. The funds are typically used for product development, marketing efforts, and building a small team to scale the business. Investors at this stage look for companies that have proven potential but need capital to fuel growth.

Advantages of Seed Funding:

Provides the capital needed to test and refine the product or service.

Allows for growth and market penetration.

Attracts investors who can add strategic value beyond just capital.

Disadvantages of Seed Funding:

Loss of equity as investors expect a return on their investment.

Requires a well-thought-out business plan and market strategy.

Competitive stage, as many startups are also seeking seed funding.

Series A Funding: Scaling Your Business

Series A funding is typically sought after a startup has achieved product-market fit and is generating consistent revenue. The main goal of this funding round is to scale the business by expanding the team, improving the product, and ramping up marketing efforts.

At this stage, venture capital firms are typically the key investors. They seek startups with proven business models, revenue growth, and scaling potential. Investors at this level expect detailed plans for scaling and a strategy to capture larger market share.

Advantages of Series A Funding:

Access to larger amounts of capital to scale operations.

Expertise and mentorship from experienced investors.

Enhanced credibility in the market.

Disadvantages of Series A Funding:

Loss of more equity in the company.

Higher expectations from investors for rapid growth and scalability.

Increased pressure to meet performance milestones.

Series B Funding: Expanding Your Market Share

Series B funding is sought by startups that have already achieved significant growth and are looking to expand their market share. At this point, your company has proven that its business model works, and investors are willing to support your efforts to scale even further.

Funds from Series B are used for larger expansions, such as entering new markets, increasing staff, and developing new products or services. Investors in this round include venture capital and private equity firms, and corporate investors. They seek high-growth companies with a proven track record.

Advantages of Series B Funding:

Provides significant capital to fuel rapid growth.

Expands the company’s reach and operations.

Attracts experienced investors with deep industry knowledge.

Disadvantages of Series B Funding:

Even more equity may be given up to investors.

Competitive stage, as successful companies attract a lot of attention from VCs.

Increased pressure to perform and meet high expectations.

Series C Funding: Preparing for Global Expansion

At this stage, your startup is likely a leader in its industry, with established revenue streams and a solid market presence. Series C funding is primarily used to fuel global expansion, acquisitions, or the development of new product lines.

Series C raises a large amount of capital. It comes from late-stage venture capital, private equity firms, and hedge funds. These investors are looking for established companies with a track record of success and growth potential in new markets.

Advantages of Series C Funding:

Enables global expansion and market diversification.

Provides significant resources to innovate and acquire other companies.

Attracts institutional investors and large firms with deep pockets.

Disadvantages of Series C Funding:

Even less control for the original founders.

Complex regulatory and legal considerations as the company grows.

The pressure to continue expanding and innovating.

Series D and Beyond: Fueling Continued Growth

Not all startups pursue Series D funding. For those that do, it means they want more capital to grow, enter new markets, or prepare for an IPO (Initial Public Offering). Series D and beyond are less common and are usually reserved for companies that need substantial amounts of capital to reach their goals.

Advantages of Series D Funding:

Provides additional capital to continue growing.

Often used to prepare the company for IPO or a significant exit.

Attracts institutional investors looking for a late-stage investment opportunity.

Disadvantages of Series D Funding:

Dilution of ownership continues with additional rounds.

Investors may expect immediate returns or rapid growth.

The company faces increased pressure to perform in a competitive market.

Initial Public Offering (IPO): Going Public

An IPO is a major milestone for any company. It involves offering shares to the public for the first time, making the company publicly traded on a stock exchange. The primary benefit of an IPO is raising significant capital and providing liquidity for early investors.

An IPO brings many challenges. These include more regulatory scrutiny, market pressures, and a loss of control as shareholders now own a stake in the company. The company must meet rigorous financial reporting standards, and its performance is subject to the whims of the stock market.

Advantages of an IPO:

Provides large capital influx to fund further expansion.

Increases public visibility and credibility.

Liquidity for investors and founders.

Disadvantages of an IPO:

Increased scrutiny and regulatory compliance.

Loss of control as the company becomes subject to shareholder interests.

High costs associated with going public.

Mergers and Acquisitions (M&A): Exit Strategy for Investors

Mergers and acquisitions (M&A) are common exit strategies for startups. If a startup is acquired by a larger company or merges with another, investors and founders can receive a profitable exit. M&A deals can provide funds for growth. But, they can change the company’s direction and culture.

Advantages of M&A:

Provides liquidity and exit opportunities for investors and founders.

Can lead to more significant growth and market opportunities.

Allows startups to gain access to additional resources and networks.

Disadvantages of M&A:

Potential loss of company culture.

Loss of autonomy and control over business decisions.

Integration challenges with the acquiring company.

Alternative Funding Options

Startups can explore alternative funding, like venture debt, grants, or corporate venture capital. This is in addition to the traditional funding stages above. Each of these options has its own set of advantages and challenges and may be appropriate for different business needs and goals.

Any entrepreneur must know the startup funding stages. It’s key to raising capital and scaling their business. Startups can confidently navigate the complex funding landscape. They should align funding strategies with the specific needs and goals of each stage. Whether you are bootstrapping, seeking seed funding, or preparing for an IPO, knowing when and how to secure capital can help you build a sustainable and successful business.

In India’s fast-changing startup scene, picking the right business structure is vital. Among various options, the Limited Liability Partnership (LLP) is now a popular choice. It is especially favored by small and medium-sized enterprises. This blog delves into the essence of LLPs, their incorporation process, taxation framework, benefits, and a comparative analysis with Private Limited Companies (Pvt Ltd), highlighting why an LLP might be the optimal choice for your business.

What is an LLP?

A Limited Liability Partnership (LLP) is a hybrid business. It combines the benefits of partnerships and companies. It offers the flexibility of a partnership firm and the limited liability feature of a company, ensuring that partners are not personally liable for the firm’s debts beyond their agreed contribution. This structure provides a separate legal identity, perpetual succession, and the ability to own property in its name.

Incorporation of an LLP in India

Incorporating a Limited Liability Partnership (LLP) in India requires a process. This ensures compliance with the law and readiness to operate. Here’s a structured guide to the key steps involved:

Obtain Digital Signature Certificates (DSC):

All designated partners must get a DSC. The Ministry of Corporate Affairs (MCA) requires digital signatures on electronic documents.

DSCs can be obtained from government-recognized certifying agencies.

Reserve LLP Name:

Propose a unique name for the LLP and check its availability on the MCA portal.

Submit the selected name for approval through the ‘Reserve Unique Name’ (RUN-LLP) service.

File Incorporation Documents:

Prepare and file the incorporation document using Form FiLLiP (Form for Incorporation of Limited Liability Partnership) with the Registrar of Companies (RoC).

Attach necessary documents. These are:

Proof of registered office address.

Subscriber’s sheet.

Partner consent forms.

Obtain Certificate of Incorporation:

The ROC issues the Certificate of Incorporation, confirming the LLP’s status, after verification.

Execute LLP Agreement:

Draft the LLP Agreement outlining the rights and duties of partners.

File the agreement with the RoC within 30 days of incorporation.

Taxation of LLPs in India

LLPs in India are taxed similarly to traditional partnership firms. The key aspects of LLP taxation include:

Income Tax Rate:

INCOME

TAX RATE

SURCHARGE

CESS

Upto 1cr

30%

NIL

4%

More than 1cr

30%

12%

4%

Alternate Minimum Tax: LLPs are subject to AMT at 18.5% of adjusted total income if the regular income tax payable is less than AMT.

Profit Distribution: One significant advantage is that the share of profits distributed to partners is exempt from tax in their hands, avoiding double taxation.

Taxation Benefits of LLPs

LLPs offer several tax benefits that make them an attractive business structure:

No Dividend Distribution Tax (DDT): LLPs in India are not subject to Dividend Distribution Tax (DDT). This exemption allows LLPs to distribute profits to their partners without the additional tax burden that companies face when distributing dividends to shareholders.

Deductions on Remuneration: You can deduct payments like salary, bonus, and commissions from the LLP’s income. This lowers its taxable income.

Exemption from Deemed Dividend: Income tax laws’ deemed dividend rules do not apply to LLPs. This prevents extra tax liabilities.

LLP vs. Private Limited Company: A Comparative Analysis

When deciding between an LLP and a Private Limited Company, consider the following factors:

Tax Rates: Private Limited Companies with a turnover up to ₹400 crore are taxed at 25%, and those exceeding ₹400 crore at 30%. Also, companies may choose concessional tax rates of 22% (for existing companies) and 15% (for new manufacturers) if they meet certain conditions. In contrast, LLPs are taxed at a flat rate of 30%, with a surcharge applicable only if income exceeds ₹1 crore.

Profit Distribution: Companies face DDT on dividends to shareholders, causing double taxation. LLPs distribute profits to partners without additional taxes, enhancing tax efficiency.

Compliance Requirements: LLPs have fewer rules than Private Limited Companies. This means less admin work and lower costs.

Case Study:

Assuming both Business A (LLP) and Business B (PLC) have a profit of ₹10 lakh:

Business A (LLP):

Income Tax (30%): ₹3,00,000

Health & Education Cess (4%): ₹12,000

Total Tax: ₹3,12,000

Profit After Tax: ₹6,88,000

Profit Distribution: Tax-free in partners’ hands.

Business B (PLC):

Corporate Tax (25%): ₹2,50,000

Health & Education Cess (4%): ₹10,000

Total Tax: ₹2,60,000

Profit After Tax: ₹7,40,000

Dividend Distribution: Dividends taxed at shareholders’ applicable income tax rates.

Analysis:

At first glance, the PLC appears to have a lower tax liability, resulting in higher post-tax profits. However, when distributing these profits as dividends, shareholders are taxed at their respective income tax rates, potentially reducing their net income.

The LLP has a higher initial tax rate. But, profit distributions to partners are tax-exempt. This can save taxes, especially for high-income partners.

India’s LLPs are ideal for startups and SMEs. They offer flexibility, tax efficiency, and low compliance. LLPs have big advantages over Private Limited Companies. They have no Dividend Distribution Tax. They can distribute profits tax-free. Their regulations are simpler. Your choice should align with your business goals. LLPs are a smart option for those who prioritize low cost and simplicity. Choose wisely to unlock your business’s true potential!

Tax harvesting is a strategic way to save on taxes by selling investments to either book gains or losses. The idea is to reduce your overall tax burden by carefully timing these transactions. You can offset gains with losses or make use of tax exemptions provided under the Income Tax Act. In India, tax harvesting is common for equity investments and mutual funds. Capital gains taxes can have a big impact.

Methods of tax harvesting:

Tax-Loss Harvesting:

Identify underperforming assets: Review your investment portfolio and identify positions that are at a loss. These can be individual stocks, mutual funds, or exchange-traded funds (ETFs).

Sell at loss: Sell the investments that are at a loss to realize the loss. This can offset any capital gains you’ve realized in other investments, reducing your taxable income.

Offset capital gains: The losses can offset both short-term and long-term capital gains. However, long-term capital losses can only offset long-term capital gains, while short-term capital losses can offset both short-term and long-term capital gains.

Reinvest: Tax-loss harvesting can also be a good opportunity to rebalance your portfolio. If you sell a losing investment, consider reinvesting in a mix of other investments. This will help maintain your asset allocation. When tax harvesting, remember that equities use FIFO for sales. It means the oldest shares are sold first. The average price is not taken into consideration.

Loss Carry-forward: Losses can be carried forward for up to 8 years from the year they were incurred. However, if the return is not filed by the due date, the losses cannot be carried forward.

Long-Term Capital Gains Tax Harvesting:

Since LTCG tax applies to capital gains above ₹1.25 lakhs, you can reduce your tax liability by limiting your gains. Monitor your gains and consider selling the investment before they exceed ₹1.25 lakhs.

Description

Amount (₹)

Total Sale Amount

₹10,00,000

Cost of Investment

₹7,50,000

Long-Term Capital Gain

₹2,50,000

Exempted Limit (₹1.25 Lakhs)

₹1,25,000

Taxable Gain (Exceeding ₹1.25 Lakhs)

₹1,25,000

LTCG Tax Rate (12.5%)

12.5%

LTCG Tax Rate (12.5%)

₹15,625

Instead of selling ₹10 lakhs worth of equity, you can sell ₹8.75 lakhs worth to incur no LTCG tax.

The 2024 Budget has introduced the following changes: The exemption limit for Long-Term Capital Gains on transfer of equity shares, equity-oriented units, or Business Trust units has been raised from ₹1 lakh to ₹1.25 lakh per year. However, the tax rate has increased from 10% to 12.5%.

Benefits of Tax Harvesting:

Reduce Taxable Income: Tax-loss harvesting helps lower your overall tax liability by offsetting capital gains with capital losses, reducing the amount of taxable income

Maximize After-Tax Returns: By lowering your tax bill, tax harvesting allows you to keep more of your investment returns, enhancing your overall after-tax returns.

Strategic Portfolio Rebalancing: Selling underperforming assets provides an opportunity to rebalance your portfolio, ensuring it aligns with your investment goals while minimizing tax impact.

In conclusion, tax harvesting is a smart strategy. It can reduce your taxes and keep your investments on track. By carefully managing gains and losses, you can maximize your returns and maintain a balanced approach to tax planning. It’s a quiet yet effective way to ensure that your money is working as efficiently as possible.

SME IPOs has seen massive growth in recent years. In FY2023-24, a record 196 SME IPOs raised over Rs 6,000 crore, with 159 IPOs raising more than Rs 5,700 crore by October 2024. However, this rapid growth has raised concerns. There are issues of fund diversion, inflated revenues, and misuse of proceeds. To address these concerns and protect investors, the SEBI has introduced new rules for SME IPOs. They aim to ensure greater transparency and market integrity.

What is an SME IPO?

An SME IPO lets small and medium-sized businesses raise capital. They do this by offering shares to the public on stock exchanges for SMEs, like BSE SME and NSE Emerge. They are for smaller companies. This makes it easier for them to raise capital to grow.

Key Differences Between SME IPOs and Mainboard IPOs

Size and Scale: SME IPOs are for smaller companies, with paid-up capital under Rs 25 crore. Mainboard IPOs are for larger companies.

Regulations: SME IPOs have less stringent compliance requirements than Mainboard IPOs .

Investor Base: SME IPOs attract retail and small institutional investors. Mainboard IPOs target a wider range of investors.

Listing Platforms: SME IPOs are on dedicated platforms like BSE SME and NSE Emerge. Mainboard IPOs are on major exchanges like the NSE and BSE.

Recent Surge in SME IPOs

In just the first half of FY2024 (until October 15), 159 SME IPOs raised more than Rs 5,700 crore. Many of these IPOs were oversubscribed by large margins—some oversubscribed more than 700 times.

For instance, Rajputana Biodiesel’s IPO was oversubscribed 718 times. Apex Ecotech’s was oversubscribed 457 times. Lakshya Powertech’s was oversubscribed 573 times.

While the growing interest in SME IPOs reflects a strong investor appetite, it also raises concerns. SEBI’s data shows that the applicant-to-allotted investor ratio increased significantly. It rose from 4 times in FY2022 to 46 times in FY2023, and 245 times in FY2024. This rise in investor participation shows the risks of fraud. It also highlights the need for tighter regulations.

Concerns Around SME IPOs

While SME IPOs have helped many businesses raise capital, they have also raised several concerns:

Promoter-Controlled Entities: Many SME IPOs are by familyor promoter-controlled firms with concentrated ownership. This limits the influence of independent investors or private equity, who usually help keep the promoters in check.

Diversion of Funds: Some companies have diverted IPO proceeds to related parties and shell companies. Some companies have engaged in circular transactions. They recorded sales and purchases among related parties to inflate revenues and create a false image of growth.

Inflated Revenues: Some companies mislead investors by inflating revenues through circular transactions.

SEBI has been actively investigating and acting against companies that misuse IPO funds. For example, it recently cancelled the IPO of Trafiksol ITS Technologies. The IPO had been oversubscribed 345.65 times. This was after discovering evidence of fund misuse through shell companies. SEBI also instructed the company to refund the money to investors.

New SEBI Regulations for SME IPOs

On December 18, 2024, SEBI introduced new eligibiliy criterias to improve the framework for SME IPOs. These measures aim to protect investors and ensure market integrity. They allow only financially sound and transparent SMEs to access public capital markets.

Key Changes in SEBI’s New Regulations:

Profitability Requirement: SMEs must have operating profits of at least ₹1 crore in two of the last three years before applying for an IPO.

Cap on Promoter Offer for Sale (OFS): Promoters can only sell up to 20% of the issue size during the IPO and no more than 50% of their total holdings.

Restriction on Loan Repayment: IPO proceeds cannot be used to repay loans from promoters, related parties, or promoter groups.

Cap on General Corporate Purposes (GCP): A maximum of 15% of the total amount raised, or ₹10 crore (whichever is lower), can be allocated for general corporate purposes.

These new rules aim to prevent misuse of proceeds. They ensure that only companies with strong finances and clear operations can enter the public market.

The Future of SMEs in India

Despite these concerns, the future of SMEs in India looks promising. Government initiatives like Startup India and Make in India, and a rise in tech for compliance and reporting, are helping SMEs. As more SMEs use digital tools to improve operations and reporting, the SME IPO market should grow further. This will offer great opportunities for businesses and investors.

However, as the market continues to expand, it’s crucial that SEBI’s new regulations are followed to ensure that the sector remains transparent, trustworthy, and sustainable. With these new safeguards in place, SMEs can access the public market in a way that promotes investor confidence and ensures long-term growth.

Understanding the taxation of online gaming in India has become increasingly important as the industry has grown rapidly, transforming from a niche hobby into a multi-billion-dollar sector. This rapid growth has led the Indian government to impose specific tax rules to ensure oversight and revenue collection.

Understanding these tax implications is crucial for gamers, developers, and investors alike.

This article will explore key tax rules for India’s online gaming industry. It will cover income tax on winnings, GST changes, corporate tax, and the skill vs. chance games debate.

How Online Gaming is Categorized

In India, taxation of online gaming revolves around two primary distinctions: games of skill and games of chance.

Games of Skill: Platforms hosting skill-based games, like fantasy sports (Dream11, MPL) and card games (RummyCircle), argue their games rely on player knowledge and strategy, not luck. They are skill-based intellectual activities and not gambling.

Games of Chance: These include online lotteries, poker, or casino-style games, often considered gambling. Such activities face stricter scrutiny and higher tax rates.

This distinction has been legally challenged and upheld in several cases, notably a Supreme Court ruling involving Dream11. The court ruled that fantasy sports platforms like Dream11 are games of skill, not chance. So, they are exempt from gambling laws.

But, the classification still remains a grey area. Disputes continue between game developers and regulators.

Tax on Online Gaming

Income Tax on Winnings

Taxability

Prize money from online gaming is taxable under Section 115BB of the Income Tax Act at a flat 30%, regardless of total income. No deductions (except TDS) are allowed.

TDS Deductions

Section 194BA mandates that online gaming platforms deduct TDS at 30% on net winnings at year-end or upon withdrawal, whichever is earlier.

The previous rules exempted winnings up to ₹10,000. That exemption is gone. TDS now applies to all winnings, no matter the amount.

Set-Off of Losses

The IT Act does not explicitly ban offsetting losses from one game against profits from another. But, tax practices usually calculate net winnings without such adjustments.

However, losses in the same year may be set off across income sources, except where specific restrictions apply, such as carrying forward losses to subsequent years.

Expenditure Deduction

The IT Act, section 58(4), disallows deductions for expenses from online gaming. This applies to lotteries, crossword puzzles, card games, and other games. Their costs are non-deductible.

GST on Gaming Platforms

A flat GST rate of 28% is now levied on the full face value of bets, stakes, or entry fees for all online games, whether skill-based or chance-based.

This uniform rate replaces the previous GST structure, which applied 18% GST for skill-based games and 28% GST for chance-based games.

Corporate Taxes for Gaming Companies

Gaming companies operating in India must adhere to corporate tax regulations. Profits are taxed at prevailing corporate tax rates. Companies with international operations must comply with transfer pricing rules.

The Future of Gaming Taxation in India

As the gaming industry continues to evolve, so will its taxation framework. Potential areas of focus include:

Clearer regulations for in-game cryptocurrency transactions.

Streamlined taxation for international gaming platforms.

Enhanced systems for tax collection and compliance.

Policymakers will likely engage with industry stakeholders to create a balanced approach that fosters growth while ensuring fair taxation.

The tax laws for India’s online gaming industry can be tough to navigate. But, staying informed is key to compliance and success. Whether you’re a gamer turning professional, a developer building the next big game, or an investor eyeing the market, a thorough understanding of tax obligations and benefits can have a major impact on your journey. As the industry levels up, so does the importance of mastering its financial rules. Embrace the challenge. Let your passion for gaming thrive in India’s changing tax environment.

Governments try to boost the economy, improve the balance of payments, and increase jobs. For this, the government tries to increase its exports by providing various reliefs to exporters. One of the reliefs provided by the government under the GST regime for increasing exports is Zero Rated Supply.

Introduction

Export supplies of a taxpayer registered under GST are classified as zero-rated supplies. Zero-rated supplies under GST are eligible for a refund. Taxpayers are required to furnish all details of zero-rated supplies in GSTR-1 and GSTR-3B.

What is Zero Rated Supply?

As per Section 16 of the IGST Act, zero-rated supply means:

Export of goods or services, or both;

Supply of goods or services, or both, to a Special Economic Zone developer

Supply of goods or services, or both, to a Special Economic Zone unit.

The Finance Bill 2021 amended the definition of zero-rated supply to include-

Transactions of supply to SEZ only when the said supply is for authorized operations.

Foreign exchange remittance will be linked in case of export of goods with the refund.

Refund under Zero-Rated Supply

There are two option available with the suppliers making the Zero-rated Supplies to claim refund for the input tax paid on the goods and services :-

The dealer can export goods or services under Bond or LUT, without paying IGST. They can then claim a refund of the accumulated Input tax credit.

The dealer can pay IGST on supplies of goods or services. They can then claim a refund.

For example, an exporter supplies pen to Dubai and uses ink in the production of pen. The exporter has an option to claim input tax credit of the GST paid on the purchase of ink or can claim refund of Tax paid.

The dealers are provided with a flexibility to choose between any two options as per their convenience.

Amount of Refund

In case of zero-rated supply of goods or services or both without payment of tax under bond or letter of undertaking in accordance S.16(3) of the IGST Act, refund of ITC shall be granted as per the following formula:

Refund Amount = (Turnover of zero rated supply of Goods + Turnover of zero rated supply of services) * Net ITC / Adjusted Annual TurnoverWhere,

“Refund amount” means the maximum refund that is admissible

“Net ITC” means ITC availed on inputs and input services during the relevant period;

“Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax Bond/LUT.

“Turnover of zero-rated supply of services” means the value of zero-rated supply of services made without payment of tax under Bond/LUT, calculated in the following manner, namely: -Zero-rated supply of services is the aggregate of the payments received during the relevant period for zero-rated supply of services and zero rated supply of services where supply has been completed for which payment had been received in advance in any period prior to the relevant period reduced by advances received for zero rated supply of services for which the supply of services has not been completed during the relevant period;

“Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under subsection (112) of section 2, excluding the value of exempt supplies other than zero-rated supplies, during the relevant period;

“Relevant period” means the period for which the claim has been filed.

Procedure to claim refund under Zero rated supply:

In case of Goods

There is a set procedure to claim refund under zero rated supply. In the case of refund for goods there is no need to file the FORM GST RFD-01 as the shipping bill itself is considered as the refund claim.

But there are two conditions to be satisfied by the shipping bill to be considered as the refund claim. These are as follows:

The person exporting the goods shall file the export manifest;

The person exporting the goods should have filed the GSTR 3 and 3B as and when needed.

If the above two conditions are fulfilled then, the refund is successfully initialized by the department.

In case of Services

In case of refund to be claimed for services the claim for refund has to be filed in form GSTR RFD – 01. For exporters of services, the following are required to be filed along with the refund claim:

A Statement containing Number and Date of Invoices; and

Bank Realization Certificates / Foreign Inward Remittance Certificates

In case of the supplier of goods or services to an SEZ

A Statement containing Number and Date of Invoices; and

Proof of Receipt of goods or services which is authorized by the specified officer of SEZ.

Details of payment made.

The declaration that the SEZ or developer of SEZ has not claimed the input tax credit of the taxes paid by the supplier.

Provisional Refund

The exporters and suppliers of SEZ are entitled to a 90% refund on a provisional basis. Provisional refund is granted within seven (7) days of the refund claim. The amount of provisional refund is credited directly to the claimant’s bank account. There is a condition attached to provisional refunds. The provisional refund is not granted if the applicant has been prosecuted for any offense under the GST law or earlier law within past five (5) years. The amount of tax evaded in such prosecution shall be more than Rupees Two Hundred and Fifty Lakhs (Rs. 2.5 Crores).